The cost picture is simpler once you split it into four parts

- The free tier has no monthly fee, but card payments still carry processing charges.

- Pro costs $15 per month billed annually; Team costs $35 per month billed annually.

- Pro and Team share the same card fee, but Team has the cheapest eCheck option and more operational features.

- Standard withdrawals to a bank account are free, while instant transfers cost extra.

- Cash and check payments can be recorded with no platform fee.

- By default, payers cover the transactional fee, but organizers can change that setting.

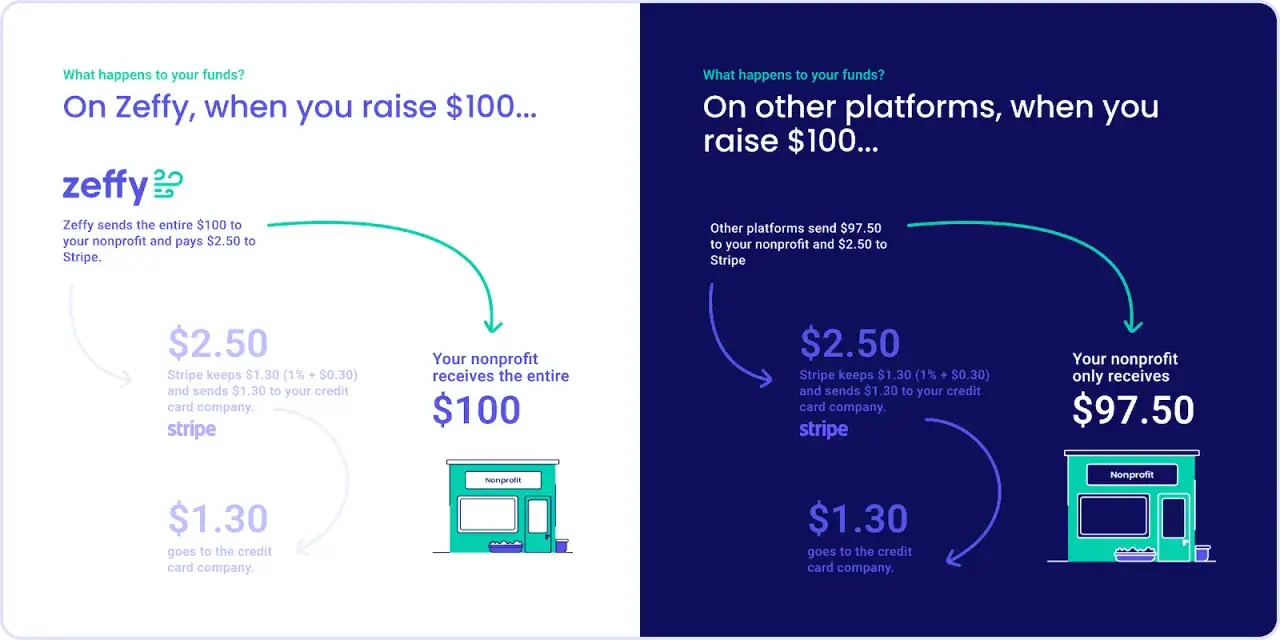

How Cheddar Up charges a nonprofit

I think about this platform’s pricing in two layers. First is the plan itself: Free Forever, Pro, Team, or Partner. Second is the transactional layer, where card fees, eCheck fees, and optional instant transfers show up; Cheddar Up's help center also makes clear that standard bank withdrawals do not carry a withdrawal fee.By default, the payer covers the convenience fee, but organizers can absorb it, split it, or offer the choice at checkout. That matters for nonprofits because it lets you decide whether you want to protect the budget, keep donor friction low, or strike a middle ground. Once that structure is clear, the plan comparison becomes much easier to read.

What each plan gives you for the monthly price

Here is the part most teams want first: the published price and what you actually get for it. I would read this table as a budget tool, not a feature brochure, because the cheaper plan is only cheaper if it still fits the way your group collects money.

| Plan | Monthly price | Card processing fee | eCheck fee | Best fit |

|---|---|---|---|---|

| Free Forever | $0 | 3.95% + $0.95 | Not available | Simple collections, cash/check recording, peer-to-peer fundraising, and groups that want no monthly commitment |

| Pro | $15/month billed annually | 3.59% + $0.59 | 1.59% (minimum $1) | Groups that need eCheck, waivers, shipping, taxes, discount codes, custom receipts, or file uploads |

| Team | $35/month billed annually | 3.59% + $0.59 | $0.95 flat | Nonprofits that need branding, waitlists, unlimited managers, reporting, integrations, or tax-deductible receipts |

| Partner | Custom | Custom | Custom | Multi-level organizations that need templates, oversight, and dedicated onboarding |

The key detail is that Pro and Team share the same published card fee, so the real difference is operational rather than transactional. That means the upgrade decision is usually about workflow, not just cents per payment. The checkout math shows why that matters.

What a real checkout costs in practice

I like to test pricing with simple examples because a fee looks small until it repeats across dozens of parent payments, dues, or donation entries. The table below assumes the organizer absorbs the fee rather than passing it through to the payer.

| Transaction size | Free plan card fee | Pro or Team card fee | Pro eCheck | Team eCheck |

|---|---|---|---|---|

| $10 | $1.35 | $0.95 | $1.00 | $0.95 |

| $25 | $1.94 | $1.49 | $1.00 | $0.95 |

| $100 | $4.90 | $4.18 | $1.59 | $0.95 |

If you let payers cover the fee, your organization spends less, but the checkout total rises for the person paying. On a $10 card payment under Pro, for example, the payer total lands around $10.98. That trade-off is why fee policy matters almost as much as the plan itself.

When the paid plans earn their keep

I would not buy Pro or Team just to save a few cents on a couple of payments. But if your group absorbs card fees and collects often, the lower per-transaction cost can offset the subscription faster than many boards expect. The question is not whether the paid plan is cheaper in isolation; it is whether it reduces enough recurring cost or admin time to justify itself.

| Average card payment | Pro breaks even against Free at about | Team breaks even against Free at about |

|---|---|---|

| $25 | 34 payments per month | 78 payments per month |

| $50 | 28 payments per month | 65 payments per month |

| $100 | 21 payments per month | 49 payments per month |

Those break-even points only matter if you are absorbing the card fee. If payers are covering it, the monthly plan cost becomes less about transaction savings and more about what the workflow features buy you: eCheck, custom receipts, shipping, taxes, branding, reporting, and fewer manual follow-ups. In nonprofit work, that hidden admin value often matters more than the spreadsheet math.

The smaller charges and edge cases worth budgeting for

The headline fee is not the only cost variable. For nonprofits that move money quickly or handle occasional disputes, these small charges can matter just as much as the posted processing rate.

| Charge | Cost | Why it matters |

|---|---|---|

| Standard withdrawal to a bank account | $0 | This is the default way to move funds out without adding another fee. |

| Instant transfer | 1.95% per transfer, minimum $1 | Useful when cash flow matters, but expensive enough to avoid as a routine habit. |

| Payment dispute | $10 non-refundable | Chargebacks are rare for many groups, but they should still be in the budget. |

| Cash/check recording | $0 | Helpful for offline collections, though the admin work shifts to tracking and reconciliation. |

According to Cheddar Up's help center, transaction fees are refunded when the original payment is refunded within 10 days, and eCheck refunds can be made within 90 days. That is a useful detail for schools and nonprofits that process event cancellations or order changes, because refund timing can quietly affect your net revenue. The practical rule is simple: keep standard withdrawals as your default, and treat instant transfers as an exception rather than a habit.

How I would budget this for a nonprofit collection

- Start with Free Forever if you only need basic collections and can live without eCheck, waivers, or advanced reporting.

- Move to Pro if you need eCheck, shipping, taxes, discount codes, or a lower card fee on recurring collections.

- Choose Team if branding, waitlists, tax-deductible receipts, integrations, or stronger reporting will save staff time.

- Let payers cover fees by default when the budget is tight, then switch to organizer-paid fees only when donor experience or campaign goals justify it.

- Avoid instant transfers unless timing matters more than the 1.95% cash-out charge.

If I were setting this up for a volunteer-run nonprofit, I would begin with the free tier, keep standard withdrawals on, and only move up when a real workflow problem appeared. The cleanest budgeting habit is to decide upfront who pays the convenience fee, because that single choice changes both the donor experience and the organization’s bottom line.