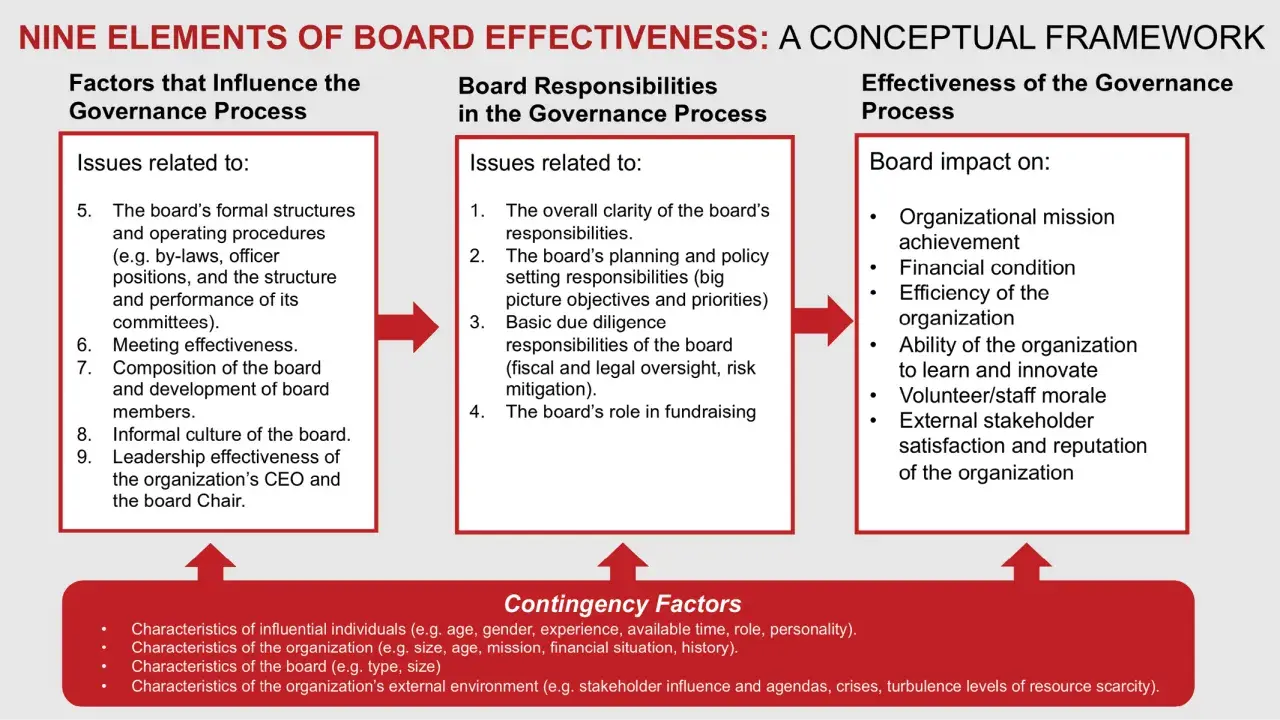

What a nonprofit board is really there to do

- Set mission, strategy, and guardrails for the organization.

- Exercise the fiduciary duties of care, loyalty, and obedience.

- Oversee budgets, risk, compliance, and key policies.

- Hire, support, and evaluate the chief executive.

- Serve as ambassadors and resource builders without micromanaging staff.

Where governance ends and management begins

I usually start with the simplest rule: the board decides the direction, and staff decides how the work gets done. When that line blurs, meetings get noisy, staff loses room to lead, and trustees end up solving problems that should have been handled operationally. I use “board” below to mean the governing body, whether your organization calls it a board of trustees or a board of directors.| Area | Board responsibility | Staff responsibility |

|---|---|---|

| Mission and strategy | Approve the mission, review long-term priorities, and make sure strategy matches purpose | Design and execute programs that advance the strategy |

| Budget and resources | Approve the budget and monitor whether resources are being used wisely | Prepare budgets, manage spending, and report results |

| Leadership | Hire, support, and evaluate the chief executive | Lead staff, operations, and daily decision-making |

| Policies and compliance | Adopt oversight policies and hold the organization accountable | Implement procedures and keep records current |

| External relationships | Open doors, build trust, and represent the mission publicly | Maintain day-to-day partnerships and communications |

That separation is not about distance; it is about accountability. Once that boundary is clear, the legal duties become much easier to see, because governance is not just a style choice. It is a standard trustees are expected to meet.

The three fiduciary duties every trustee must understand

Most of the real substance of board service sits inside three legal duties: care, loyalty, and obedience. They sound abstract until you translate them into what trustees read, question, approve, and refuse to do. In practice, these duties are the backbone of trustworthy nonprofit governance.

Duty of care

The duty of care means paying attention, asking informed questions, and making decisions with reasonable prudence. A trustee should read board packets, understand the financials, know the organization’s risks, and show up prepared. I think of it this way: if a board member has not done the homework, the vote is not really informed.

Duty of loyalty

The duty of loyalty requires trustees to put the organization’s interests ahead of personal benefit, politics, ego, or outside loyalties. That means disclosing conflicts of interest, stepping back when a matter directly affects you, and resisting the temptation to use board access for private gain. This duty is where many boards get sloppy, especially when personal relationships are strong and everyone wants to “help.”

Read Also: Board Committees - Make Them Effective, Not Just Overhead

Duty of obedience

The duty of obedience is the obligation to stay true to the mission, bylaws, governing documents, donor restrictions, and applicable law. A board that drifts into side projects or approves actions that contradict the mission is not being creative; it is breaking trust. This duty matters most when a nonprofit feels pressure to chase money or popularity in ways that pull it away from its purpose.

Those three duties show up in ordinary board behavior more than in dramatic legal moments. The next place they matter is money, because mission without financial discipline is only a wish.

Financial oversight is the board’s job, even when the treasurer leads the discussion

Nonprofit board members do not need to be accountants, but they do need to be financially curious. I expect trustees to understand where the money comes from, where it goes, how much cushion the organization has, and what would happen if a grant, donor, or government contract disappeared. That is the real meaning of stewardship.

A practical board usually keeps its eyes on a few core items:

- Approved annual budget and any major variances from it.

- Cash flow, reserve levels, and restricted versus unrestricted funds.

- Basic internal controls, such as who can authorize payments and how expenses are tracked.

- Conflict-of-interest, whistleblower, and document-retention policies.

- Form 990 review before filing, so the board knows what the public will see.

One useful habit is to make financial review routine instead of dramatic. Monthly or quarterly reporting, depending on the size and complexity of the nonprofit, gives the board time to spot patterns before they become crises. I also like boards that ask blunt questions early: Are we spending in line with mission? Do we have enough runway? What assumptions would hurt us if they turn out to be wrong?

Good financial oversight naturally leads to the next question: who is translating board expectations into operational reality, and how closely should trustees watch that work?

How trustees should hire, support, and evaluate the chief executive

The board’s relationship with the executive director or CEO is one of its most important governance responsibilities. Trustees are not there to do the executive’s job, but they are absolutely there to choose the right person, set clear expectations, evaluate performance, and intervene if leadership is failing. In strong nonprofits, that relationship is firm, respectful, and documented.

- Define the role before you recruit. A vague job description creates vague leadership.

- Set a short list of measurable priorities. Mission language is important, but it should turn into concrete goals.

- Give feedback regularly, not only when something has gone wrong. Annual evaluation works best when the board has already been tracking progress.

- Plan for succession before you need it. Even a small nonprofit benefits from knowing who can steady the organization during a transition.

BoardSource recommends an annual chief executive assessment and a board self-assessment every 2 to 3 years. I think that cadence is realistic because it forces the board to stay honest about its own performance, not just the executive’s. If the board only talks to leadership when there is a problem, oversight is already too weak.

That brings up another governance issue that boards often treat as secondary when it is actually central: who sits around the table, for how long, and with what mix of experience?

Why board composition and terms shape governance quality

When I review a board, I care less about headcount than about balance. A healthy board needs people who bring financial literacy, legal judgment, program insight, fundraising credibility, and real connection to the community served. If everyone in the room looks, thinks, and networks the same way, the board may be comfortable, but it will not be especially strong.

BoardSource’s latest Leading with Intent data reports that 95 percent of nonprofit boards have terms, 54 percent have term limits, and the most common structure is two consecutive three-year terms. I find that useful because it shows renewal is normal, not radical. Term limits are not a punishment; they are a way to keep the board fresh, reduce stagnation, and make room for new skills and new voices.

Board composition also affects what the board chooses to emphasize. BoardSource’s 2024 data suggests that setting strategy has become a higher priority than fundraising, which matches what I see in effective boards: money matters, but mission clarity matters first. A board that spends all its time chasing donations and almost no time shaping strategy is usually reacting, not governing.

- Recruit for judgment, not only for influence or personal giving capacity.

- Build in orientation so new trustees understand the mission, the numbers, and the culture.

- Rotate committee assignments so knowledge spreads instead of concentrating in one pocket.

- Look for trustees who can challenge the room politely but firmly.

- Keep the board reflective of the community the nonprofit exists to serve.

Once a board gets the right people and the right rhythm, the remaining challenge is usually not skill. It is behavior. And that is where governance quietly succeeds or quietly fails.

Common mistakes that weaken nonprofit governance

The most common board failures are rarely dramatic. They are slow, familiar, and easy to excuse. I see the same patterns over and over: trustees who confuse involvement with interference, boards that approve too much too quickly, and committees that become side rooms where accountability goes to disappear.

- Micromanaging staff instead of setting direction and reviewing results.

- Acting like a social club when the organization needs a governing body.

- Rubber-stamping budgets, contracts, or executive decisions without real questions.

- Ignoring conflicts of interest because “everyone knows everyone.”

- Leaving the executive director unsupported until a crisis forces the issue.

- Failing to review board performance, which allows weak habits to become culture.

The practical cost is not abstract. Weak boards often miss early warning signs, undercut staff morale, and lose donor confidence because the organization looks less accountable than it should. A nonprofit can still do good work with a mediocre board, but it will spend far more energy compensating for governance gaps than it should.

What I would put on the board calendar first

If I had to reduce board governance to a simple operating rhythm, I would start with four recurring items: mission review, financial review, chief executive evaluation, and board self-assessment. Those four touch every major responsibility a trustee carries, and they stop the board from drifting into a ceremonial role.

- Review the strategic plan at least once a year and ask whether it still fits reality.

- Review financials on a steady cadence so risk is visible early.

- Evaluate the chief executive annually and document goals clearly.

- Run a board self-assessment every 2 to 3 years and act on the results.

- Revisit board composition, term limits, and committee structure before problems accumulate.

That is the practical heart of nonprofit board service: protect the mission, challenge the numbers, support leadership, and stay accountable to the people the organization exists to serve. When a board does those things well, it does not just comply with governance rules, it gives the nonprofit a better chance to create real community impact.